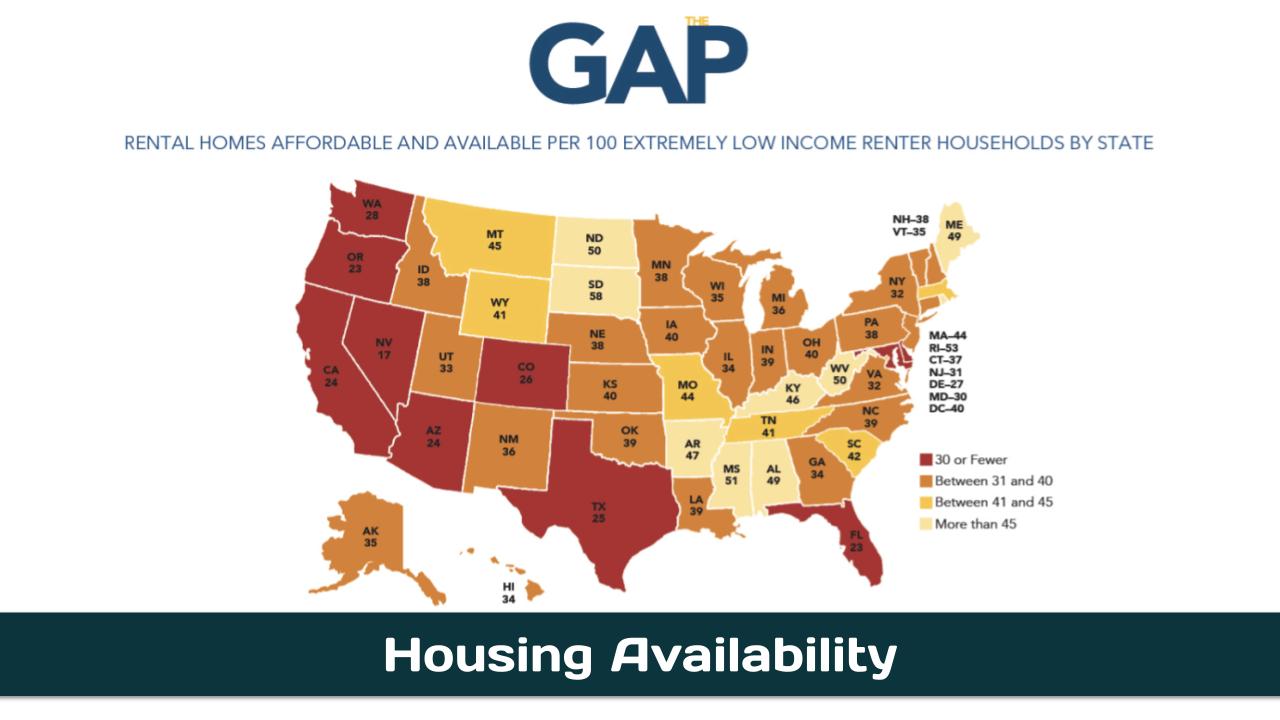

The term “Housing crisis” or “affordability crisis” is currently used in the United States and other English-speaking countries to refer to widespread shortages of housing in certain regions where people want to live. These shortages, caused in part by regulatory barriers to new construction, have had consequences such as elevated regional homelessness, housing insecurity, and high housing costs.

- In the ‘About’ section of this post is an overview of the issues or challenges, potential solutions, and web links. Other sections have information on relevant legislation, committees, agencies, programs in addition to information on the judiciary, nonpartisan & partisan organizations, and a wikipedia entry.

- To participate in ongoing forums, ask the post’s curators questions, and make suggestions, go to the ‘Discuss’ section at the bottom of the post.

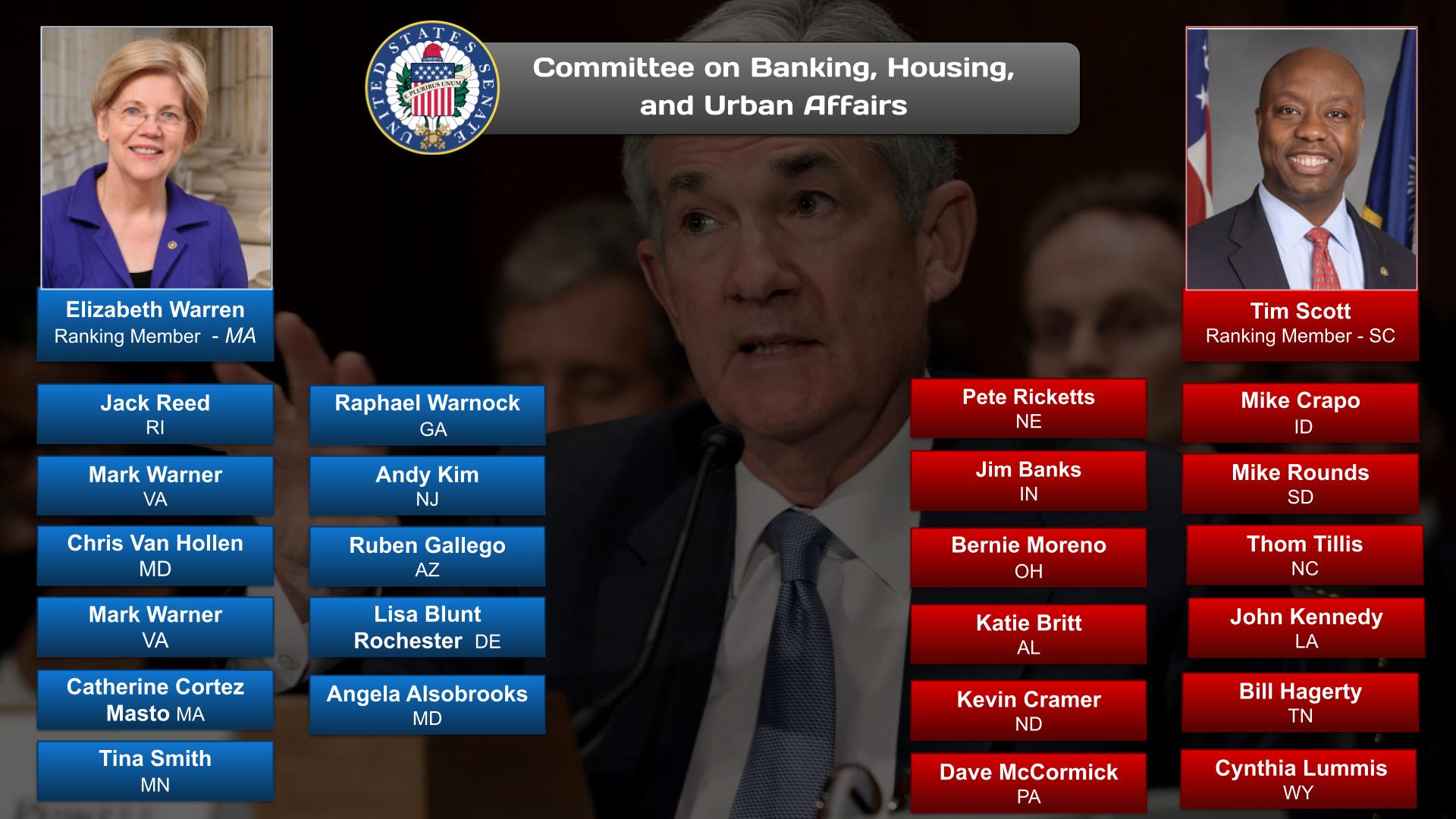

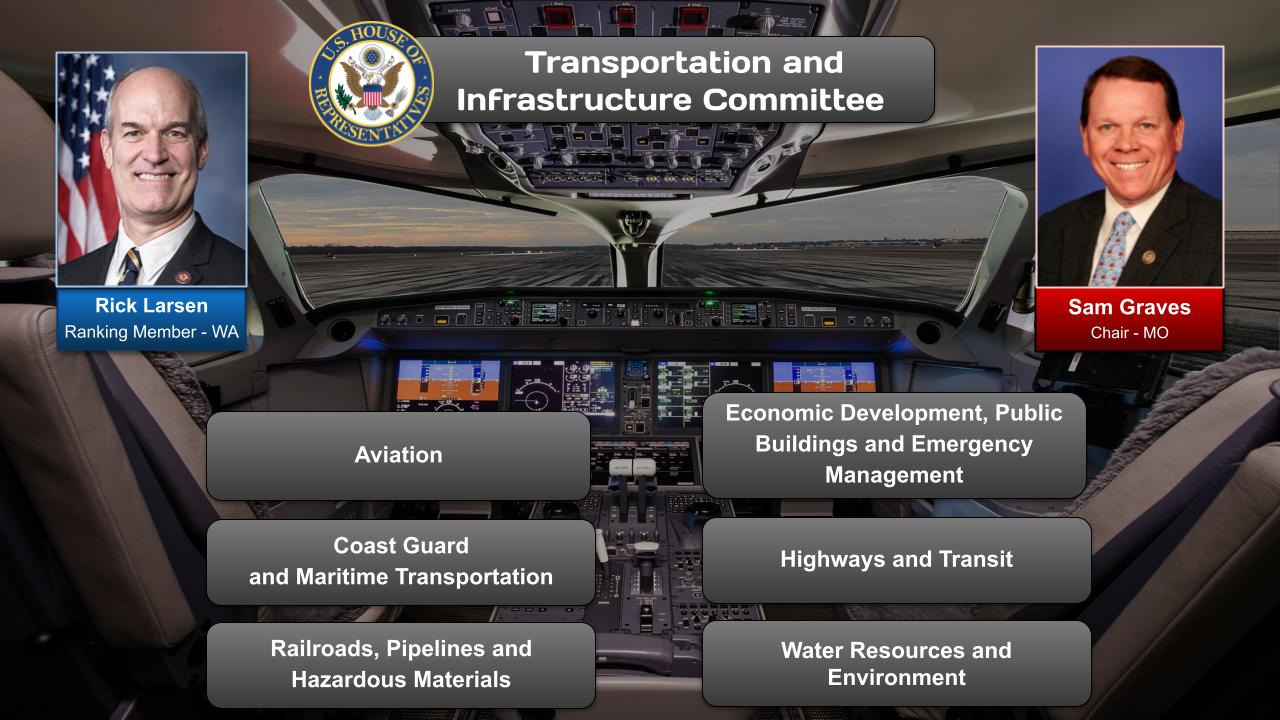

The Housing Availability category has related posts on government agencies and departments and committees and their Chairs.

PBS NewsHour – 01/06/2024 (05:36)

https://www.youtube.com/watch?v=2F40KUqazuM

Rents today are well above what they were before the pandemic. According to a recent Gallup poll, Americans’ second-highest personal finance concern this election year is the cost of housing, behind only inflation. John Yang speaks with Diane Yentel, CEO of the National Low Income Housing Coalition, about what’s keeping rents high.

OnAir Post: Housing Availability